Over the last 10 years, financial technology companies (fintechs) have experienced exponential growth, attracting over $200B in investment in 2021 alone. Several factors have created favorable conditions for fintechs to thrive; consumer adoption of digital finance has accelerated; regulators in the EU and US have broadened open-banking frameworks; and innovation in software and financial infrastructure has made starting a technology company easier than ever before.

Angela Strange—a general partner at Andreessen Horowitz—suggests that in the future, “every company will be a fintech company.”

In their annual report, McKinsey writes:

“As payments become integrated into broader customer journeys [i.e., software], the sector’s boundaries have naturally expanded … payments as a discrete experience is disappearing. The payments industry now encompasses the end-to-end money movement process, including the services and platforms enabling this commerce journey.”

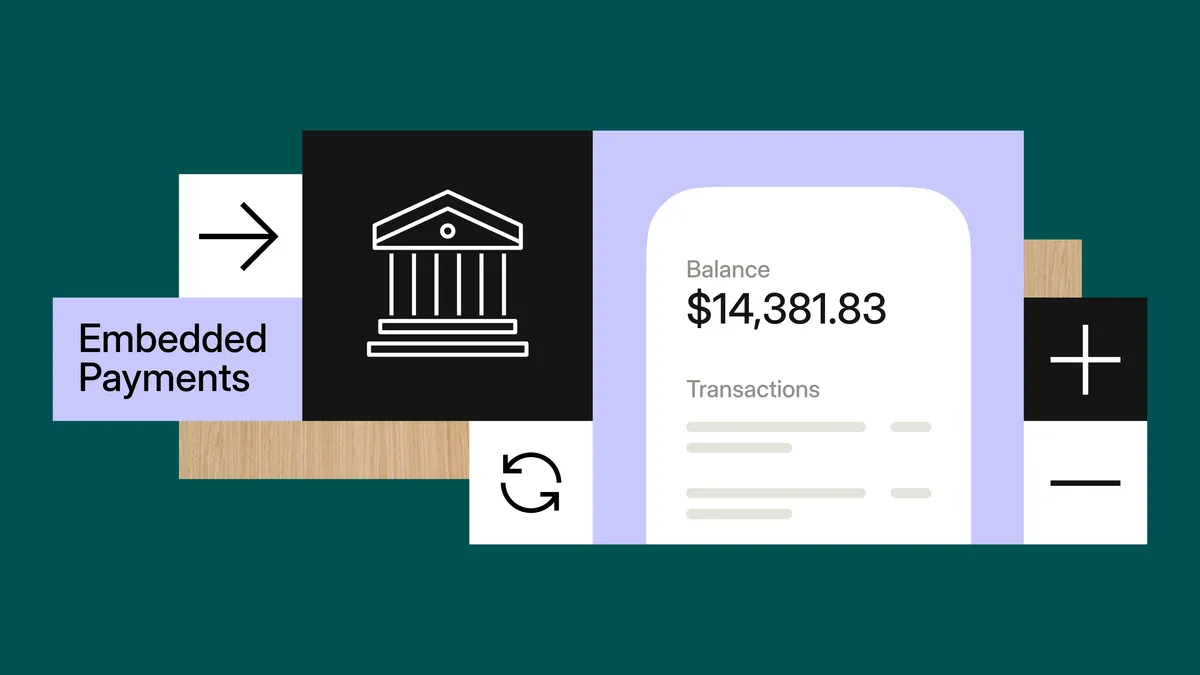

Already, software-integrated payments are ubiquitous. Consider how we travel: to pay for transportation, book lodging, order food delivery. In each case, payments are so tightly embedded within a software workflow that we forget it’s even there.

Software-integrated payments are the fastest-growing vector across the payments industry as entire industries and workflows digitalize. Global Payments noted that 60%-70% of new clients come from software channels. The industry is expected to grow to $230 billion in new revenue by 2025—an increase of 922% from 2020. It’s a $7 trillion dollar opportunity.

Over the past decade, fintech has created tremendous value by expanding access to financial services, and delivering new experiences to both businesses and consumers. It has also diminished the role of financial institutions, who have struggled to deliver compelling digital experiences to their customers. Without a sufficient response to the changing landscape, banks are leaving a significant amount of value on the table.

The challenge

Consumers and businesses have heightened expectations for their banks to deliver better tools to address their financial needs.

However, most banks have ways to go in meeting those expectations. While banks like J.P.Morgan and Goldman Sachs have made public commitments to investing in their technology to become tech-forward institutions, others have yet to make similar commitments to transformation. Such that it is, large-scale digital transformation is a complex undertaking that can take years to bear fruit, in many cases with mixed results.

Moreover, financial institutions don’t have the luxury of time when it comes to these initiatives. By 2025, neobanks like Chime and Revolut are projected to reach 20% penetration in the US. Traditional banks also face mounting pressure from a new competitive force: big tech. FAANG companies (Facebook, Amazon, Apple, Netflix, and Google) have not only gained significant market share in the payments space, but are now exploring additional, lucrative segments of banking, such as wealth management.

In such a fast-paced and complex competitive environment, banks should consider partnering with fintechs to accomplish their objectives over the next few years. Structured correctly, partnerships carry lower costs and significant upside.

What are the benefits to partnering?

Financial institutions have many strengths. Banks are safe, stable, and solvent. They provide exceptional risk expertise, access to funds that power innovation, and core financial products that undergird entire industries. Partnerships highlight these strengths by addressing potential gaps. We’ve seen three themes that make partnering with fintechs a worthwhile investment.

Support technical capabilities

The market is moving towards application programming interfaces (APIs) to support the digital capabilities that business customers expect. These include services such as treasury and liquidity management, bill payments capabilities, account opening, data aggregation, and more.

While some banks have developed sophisticated APIs for certain use cases—bill payments and treasury management services—there are still gaps. For example, there are needs for financial infrastructure to expand beyond payments to support broader commerce and payment journeys.

For many banks, partnering with a fintech company with developer-first API technology may be their best strategy to deliver a best-in-class client experience.

Expand product offering

Additionally, banks face challenges bringing new solutions to market. This is another area where fintech partnerships can help. By partnering with fintech companies, banks are able to release solutions, such as digital wallets, virtual accounts, push-to-card, request for payment (RFP), even crypto capabilities more quickly and with less resource investment.

Unlock highly-profitable customer segment

Fintech partnerships can help banks unlock new customer segments and revenue streams. Dynamic, high-growth companies in today’s economy (e.g., vertical software, fintech and marketplaces) have financial needs that extend beyond current bank capabilities. For example, platforms are often looking for integrated solutions that automate or streamline an entire business process—stitching together compliance, onboarding, payment tracking and reporting, reconciliation, ledgering and other capabilities. Banks that lack these offerings risk losing clients to other banks or third-parties.

Again, fintech partnerships here can help. Fintech partnerships offer the tools to address these clients' needs. They also signal to the market that the bank is excited to win new, dynamic clients.

Already, we’ve seen strong evidence that innovative, technology companies are a profitable client segment for banks. These companies have strong fee-revenue profiles, substantial deposits, lower loan utilization, and high growth. Banks that prioritize these segments see valuable gains when their customers become stickier with software-improved banking experiences.

How software can enable better banking experiences

As a new payment flow, software-integrated payments have distinct characteristics and needs. And these needs are simply not well-served by the available banking infrastructure today.

Our founders felt these gaps firsthand at LendingHome, building a software marketplace for real-estate borrowers. They connected the software platform to the plumbing of the banking system. And were overwhelmed by the tooling and infrastructure required to make this translation work.

In particular, they saw that payments—while important—was just one component of the digital experience. They also needed:

- Software for workflow: To onboard users, to check identities and verify accounts, to run compliance, to collect and store counterparty information. They needed software to create Nacha and wire payment files programmatically, and a robust reconciliation engine (with webhooks) to correctly track and attribute each payment throughout the banking system.

- Dashboards: To report on the business, to monitor platform activity, oversee cash balances, track failed payments, and collect approvals for transactions above a certain size. As a platform, moving other people’s money, they needed dashboards for our Client Support team to answer queries:“Hey, I don’t think the payment I’m owed has arrived yet. Where is it?”

Due to the speed of transactions, this could not be managed manually.

Why does this matter?

Software has become the front-door into our financial lives: the “new bank branch.” Activities that once took place in person or over the phone—getting a loan, making a payment, investing in a security—now occur entirely within software. Covid has only accelerated this trend. To remain a part of clients' financial lives, banks need to play well with software.

Several banks—such as Goldman Sachs Transaction Banking, JP Morgan, BMO, and US Bank, to name a few— have partnered with Modern Treasury to help mutual customers embed payments into their workflows