Over the last several years, traditional business models in financial services have been disrupted by pandemic-related consumer behavior changes, new innovations in financial technology and a more open banking regulatory framework.

Upstart innovators have taken advantage of new market gaps and delivered on evolving consumer needs with unbundled financial products, no-fee payments, direct transfers and more. Chime, with its no-fee accounts, free overdrafts and early direct deposits on paychecks, scored eight million accounts in 2020, up from just one million in 2018. Credit Karma, with its promise of helping everyone “feel confident about their finances,” has collected over 100 million users in a decade. And the much-in-the-news Robinhood, which offers commission-free investment services for stocks, ETFs and options, claimed more than 10 million accounts and billions of dollars in transaction volume this year.

As digital-first companies, these upstarts have also moved the goalposts when it comes to differentiated digital customer experiences, leveraging machine learning and advanced analytics to offer degrees of personalization and responsiveness that big banks have been slow to deliver.

Traditional institutions, who once enjoyed an entrenched base of customers to cross-sell and upsell at will, now face pressure on margins, loss of market share and customer churn. They have been slow to get rid of effort-intensive processes that make banking a chore, and they haven’t capitalized on the “direct, digital, mobile-first” model that consumers prefer. No wonder, then, that 88% of traditional banks are increasingly concerned they are losing revenue to innovators.

With deeper pockets, longer-standing customer relationships and often a century or two of industry experience working in their favor, traditional banks should be in a position to succeed. But many of these institutions are constrained by an aging operating model where processes, people and technology are aligned to functions and channels, not to the customer. Financial services organizations operating in a siloed manner aren’t able to deliver critical customer experiences that their disruptive counterparts do.

For example, a customer who visits a physical branch (silo #1) is likely to be met by a representative who doesn’t know what they’ve just browsed on digital properties like web and mobile (silos #2 and #3). Call center teams (silo #4) don’t have a record of the offer the customer received through direct mail (silo #5), and email teams (silo #6) don’t know to suppress promotional messages to the customer who just had an unsatisfactory experience with the bank’s mortgage unit (silo #7). The road to churn is paved with these siloed experiences.

Today, a handful of institutional banks are catching up, either buying or developing digital solutions for the modern economy. For example, the partnership between Chase & Zelle demonstrates a critical step towards embracing consumer convenience and digital-first banking. Progressive enterprise banks and financial services companies such as Morgan Stanley, The Hartford and Capital Group are also challenging themselves to reorganize or rebuild their operating models around the customer.

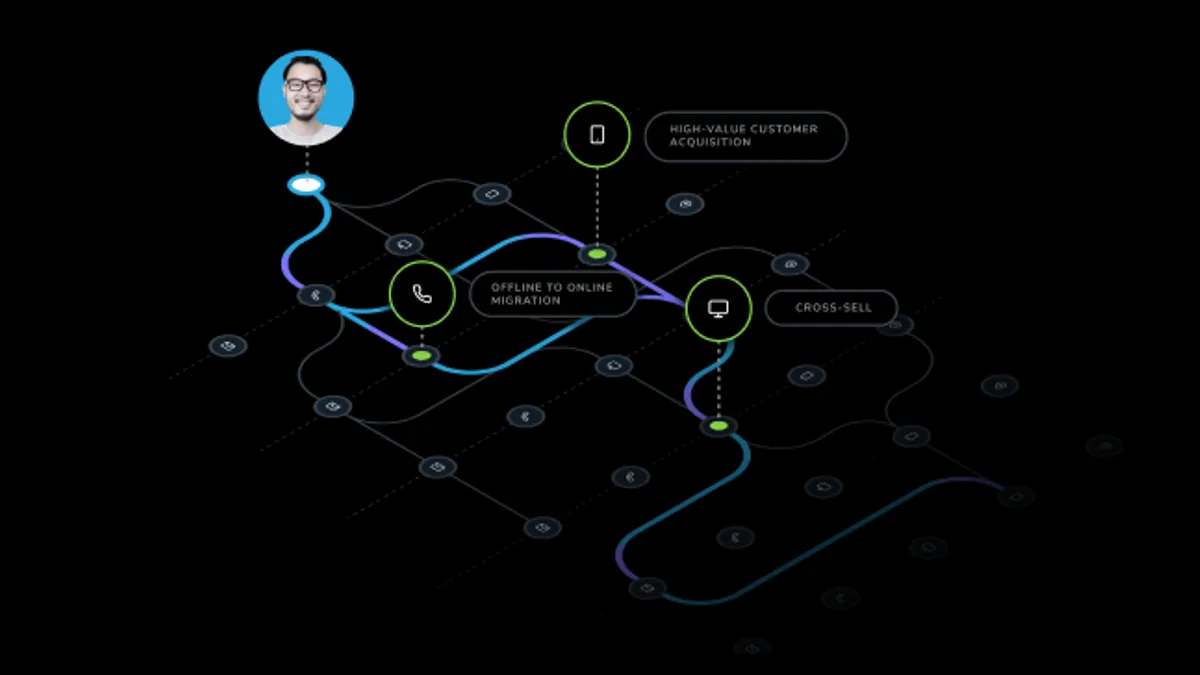

Central to a customer-centric operating model is having the organization’s people, processes and technology aligned to a single “smart hub,” not to multiple independent teams and tools. In practice, smart hubs are enabled by purpose-built customer data platforms (CDPs) and are designed to handle new, ever-more complex data formats that are unique to the activities of today’s omnichannel consumer. As such, the smart hub enables organizations to build a complete and perpetual view of each customer across channels, integrate various systems and tools to activate data seamlessly, and serve the needs of multiple business users in analyzing customer behavior and orchestrating inbound and outbound customer experiences.

Most importantly, it enables critical use cases that empower traditional institutions to compete with upstart disruptors:

- Migrate offline customers onto digital channels: Build customer journeys to educate on digital solutions and facilitate engagement across more channels, improving reach and retention.

- Improve banker awareness of customer activity: Push cross-channel behaviors to CRM systems, enabling more personalized and responsive banker engagement.

- Raise value of new customers: Model audiences for acquisition on highest LTV customers, driving growth at lower costs.

- Improve sales and servicing management: Push latest customer activities to call center advisors and sales reps, improving relevance and timeliness of engagement.

- Drive cross-sell at scale: Calculate audience affinities for specific products and launch omnichannel journeys to drive product growth.

The smart hub is emerging as the preferred approach for enterprises because it is designed for scale, flexibility and change resilience. It enables an operating model anchored by data and brought to life by the people, processes and technology that are collectively focused on delivering superior customer experiences.

If you’d like to learn more about how ActionIQ’s smart hub CDP is helping enterprise banks achieve their vision of customer-centricity with efficiency and speed, read about our solution for Financial Services.