When conversing with clients, wealth advisers tend to talk more than they realize. In an effort to get them listening more than talking, Truist has found success by using listening cards to guide advisers’ conversations with clients.

The Charlotte, North Carolina-based bank aims to “intentionally change that dynamic and really hear the client,” Brian Dowhower, Truist’s head of wealth, said in a recent interview. “It’s listening for a purpose, of hearing what the client needs you to hear.”

The cards, which the super-regional bank began using in 2022, are “a tool to help us drive that intentionality around hearing what the client needs,” he said. Since then, Truist has found success with an internal “spin-off,” using cards for sales coaching, as far as what wealth leaders need to cover with their advisers, Dowhower said.

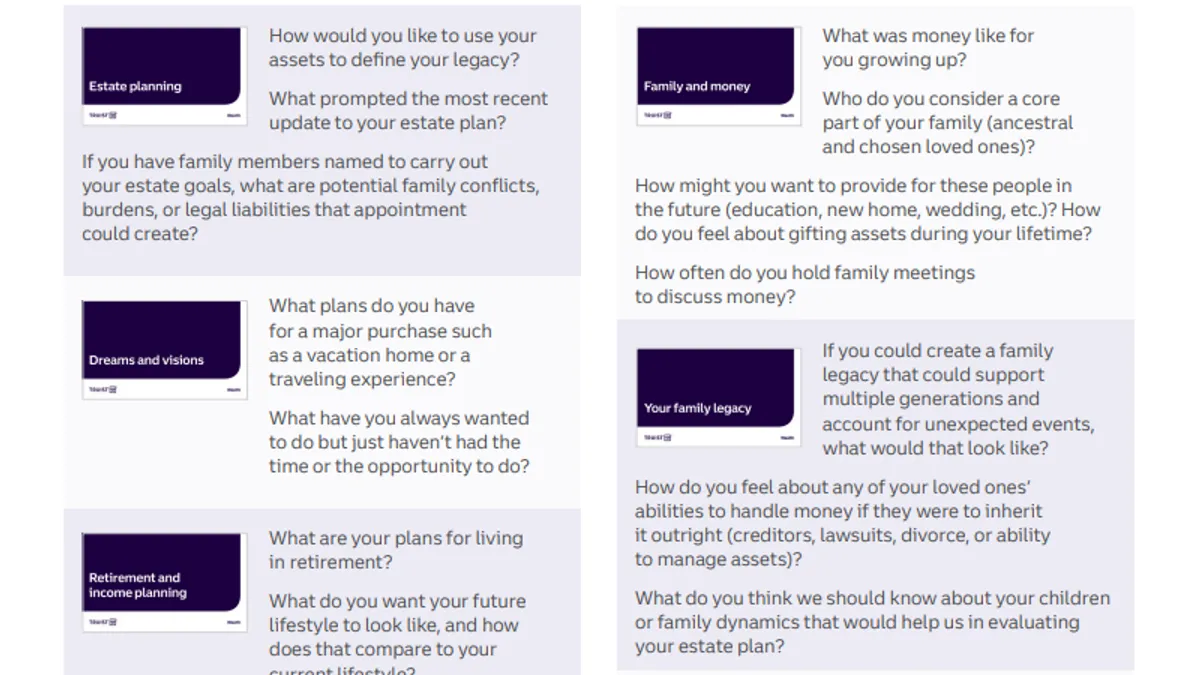

The deck of 14 cards touches on topics such as estate planning, retirement, education funding, philanthropic goals and business planning. It’s often used at initial client meetings, and an adviser might return to the cards down the road, to see if a client’s priorities have shifted or preferences have changed, Dowhower said.

The bank still has more of these conversations in person – where clients meeting with an adviser select the cards important to them – but Dowhower expects virtual meetings will soon become more common.

With the virtual experience, clients move digital cards into two columns, “now and next” and “maybe later.” Advisers pay close attention to client selections and the order they make them in – as well as what they don’t mention – trying to learn more about the “why” behind each choice. Advisers are also eager to suss out individual client interpretations of a card.

“You actually need to let them talk and let them go through it,” Dowhower said. “You don’t just say, ‘OK, you picked insurance, let me tell you about all the insurance products that we have.’ That's not the way it works. It's, ‘Why did you choose this? And what are you thinking about when you see that? And tell me more about why?’ The solution building can happen later.”

Wealth clients will sometimes treat the cards exercise like a game, trying to guess what each other might say. In some cases, couples have revealed dreams or preferences through those conversations they hadn’t yet discussed. “You’re sort of implicitly prioritizing them,” he said.

In the competitive wealth arena, $531 billion-asset Truist aims to stand out by putting “the emphasis on really listening to clients, and not pitching them something,” he said.

For advisers, “it’s a little hard for them at first,” Dowhower said. “Some pick it up easier than others. But it’s not hard because it’s complicated; it’s hard because it’s not the way that they’re trained to sell.” It’s “a very different feeling” for them, he added.

The cards also enable Truist’s roughly 1,100 wealth advisers to get a fuller picture.

“We have so many things that we can deliver, it's somewhat paralyzing to our advisers, to have to choose what the right thing is based on very limited information, and this helps them get all the information they need to position the right collective solution,” Dowhower said.

Driving profit growth

In the bank’s latest annual report, Truist CEO Bill Rogers underscored that the wealth business is key to putting the lender on a path toward bigger profits. Deepening relationships with existing clients and meeting more of their needs is one of the bank’s strategic objectives this year.

Truist’s wealth business handles asset management, trust, brokerage and investment management, and offers specialized commercial products to bank customers; wealth clients have $1 million or more in investments at the bank.

Wealth was responsible for 10% of the bank’s revenue mix in 2024; a spokesperson declined to comment on a growth target.

The wealth unit feeds Truist’s fee income, and the bank’s wealth management income rose 4% in 2024 over the prior year, to $1.4 billion, due to higher assets under management, according to the bank’s most recent annual filing.

Dowhower said he feels the weight of the wealth unit’s importance to the company.

“We have the pressure, but we also have the opportunity,” he said.

While Truist welcomes new clients, wealth has plenty of room to grow inside the bank, as existing bank customers acquire more assets over time, he said. The bank has an edge over nonbank rivals in receiving referrals from the banking side of business, he added.

To capitalize on the opportunity, Rogers has said the bank is making investments in the wealth business by adding people and resources; a spokesperson declined to quantify such investments.

Still, following Truist’s months-long effort to shave $750 million in expenses, which included workforce reductions and consolidating certain business lines, the bank continues to “intensely manage expenses,” Rogers wrote in the report.

Talent retention

Last year, Truist lost wealth advisers or teams to Fifth Third, Regions and Royal Bank of Canada. In such a relationship-focused sector, turnover can affect the bank’s efforts to grow the business, Dowhower said.

“For the same reason that we want to hire people from other places, people want to hire our folks, because they build great client relationships,” he said.

The competitive environment hasn’t changed how Truist approaches retention though, he said, adding that “people leave for idiosyncratic reasons.”

Dowhower said he sees the lender’s culture of teamwork helping to drive retention, as bank employees can make connections across business lines with the goal of expanding client relationships.

Sales leaders are actively recruiting and wealth is adding people on a regular basis, although the bank doesn’t have any targets for hiring, he said. A Truist spokesperson declined to share numbers around wealth hiring.

“We want to stay within our financial means from an expense perspective,” Dowhower said. “However, we do want to hire and we have an active pipeline.”